Bond Yields Above 5%: Is the U.S. Market Entering a New Risk Regime?

The rise in U.S. long-term bond yields above the 5% threshold marks a significant shift in the global financial landscape. For much of the past decade, markets operated in an environment defined by low interest rates and abundant liquidity. That regime supported higher equity valuations, cheap capital, and strong risk appetite. The recent move higher in yields suggests that this backdrop may be changing more structurally than previously assumed.

At the center of this shift is the repricing of inflation expectations and monetary policy. While inflation had shown signs of moderating, it has not declined sufficiently to provide central banks with confidence to ease policy aggressively. Persistent pressures from energy prices, resilient demand, and wage dynamics are forcing markets to reconsider the timing and extent of rate cuts. As a result, long-term yields are adjusting upward to reflect a more uncertain inflation outlook.

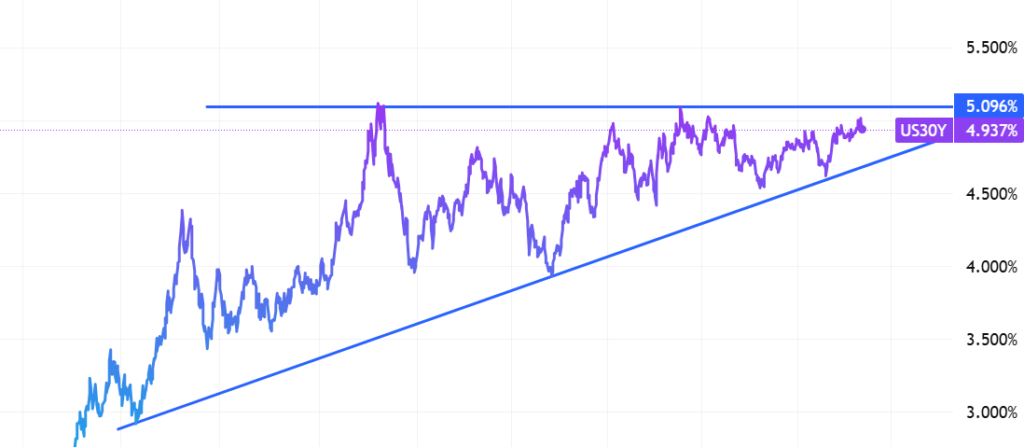

The 30-year Treasury yield crossing 5% is particularly important because it represents the market’s view of long-term economic conditions, including inflation, growth, and fiscal sustainability. Unlike short-term rates, which are heavily influenced by central bank policy, long-term yields incorporate expectations about structural risks. The recent move suggests that investors are demanding higher compensation for holding long-duration assets.

This repricing has broad implications across asset classes. In equity markets, higher yields increase the discount rate applied to future earnings, placing pressure on valuations—particularly in growth-oriented sectors. At the same time, higher borrowing costs can weigh on corporate investment and consumer spending, potentially slowing economic activity over time.

Fixed income markets are also adjusting to this new environment. Rising yields imply declining bond prices, creating mark-to-market losses for investors holding long-duration securities. More importantly, higher yields reflect tighter financial conditions, even without additional rate hikes from central banks. In this sense, the bond market itself is contributing to the tightening cycle.

Another critical factor behind rising yields is the growing concern around fiscal dynamics. Increased government borrowing, elevated deficits, and the need to finance long-term spending commitments are putting upward pressure on bond supply. As supply increases, investors require higher yields to absorb that issuance, further reinforcing the upward move in rates.

The key question is whether this shift represents a temporary adjustment or the beginning of a new regime. If inflation remains persistent and fiscal pressures continue to build, yields could remain structurally higher than in the previous decade. This would imply a sustained change in how markets price risk, capital, and growth.

However, it is important to avoid a simplistic conclusion that higher yields automatically lead to market weakness. The relationship between yields and equities is complex and depends on the underlying drivers. If yields rise due to strong economic growth, markets can absorb the increase. But if yields rise because of inflation risk and fiscal concerns, the impact is more likely to be negative for risk assets.

What is clear is that the current environment demands a reassessment of assumptions. The era of ultra-low rates may not return in the same form, and markets are beginning to adjust to that possibility. Investors who continue to rely on past frameworks risk underestimating the implications of this shift.

The crossing of 5% in long-term yields is not just a numerical milestone—it is a signal. It reflects a market that is increasingly concerned about inflation persistence, policy uncertainty, and structural imbalances. Whether this marks the beginning of a new risk regime will depend on how these forces evolve, but the direction of change is already evident.

For investors, the takeaway is clear: bond markets are no longer a passive backdrop. They are actively shaping financial conditions, influencing asset valuations, and redefining the boundaries of monetary policy. Understanding this shift is essential in navigating a market environment that is becoming more complex, more sensitive, and potentially more volatile.