Trip.com Group Limited: China’s Leading Online Travel Platform with Global Expansion Optionality

Company Overview

- Ticker: TCOM (NASDAQ)

- Headquarters: Singapore

- Founded: 1999

- CEO: Jie Sun

- Industry: Other Consumer Services

Core Business

Trip.com is China’s dominant online travel platform, offering comprehensive travel booking services across air tickets, hotels, transportation, and packaged tours.

- Accommodation Booking: Largest revenue contributor, including hotels, vacation rentals, and alternative lodging.

- Transportation Ticketing: Air, rail, and bus bookings, with strong integration across China’s travel infrastructure.

- Packaged Tours & Corporate Travel: Higher-margin offerings combining lodging, transport, and experiences, plus enterprise travel management.

- Global Platform Assets: Ownership of Skyscanner and international-facing Trip.com positions the company for outbound and inbound travel growth.

- Data & AI-Driven Personalization: Uses user data and dynamic pricing tools to improve conversion, cross-selling, and customer retention.

Industry Overview

- Supplier Concentration & Bargaining Power: Large OTAs benefit from scale-driven bargaining power with airlines and hotels, improving take rates and access to inventory.

- Marketing Intensity & Brand Moats: Customer acquisition costs are structurally high, favoring platforms with strong brands, repeat usage, and loyalty ecosystems.

- Regulatory & Data Sensitivity in China: Online travel platforms operate under data, pricing, and consumer protection regulations, adding compliance complexity but raising barriers for smaller competitors.

- Shift Toward Mobile & Super-App Integration: Travel bookings increasingly occur within mobile ecosystems, requiring deep integration with payments, maps, and lifestyle services.

- High Operating Leverage at Scale: Once fixed technology and marketing costs are covered, incremental bookings carry high contribution margins.

Key Growth Drivers

- China Travel Recovery & Normalization: Domestic and outbound travel demand continues to normalize post-pandemic.

- Market Leadership in China: Strong brand, supply relationships, and ecosystem integration create durable competitive advantages.

- Margin Expansion: Operating leverage from recovered volumes and disciplined marketing spend.

- International Optionality: Skyscanner and Trip.com international platforms provide non-China growth exposure.

- Strong Balance Sheet: Net cash position supports resilience through travel downturns.

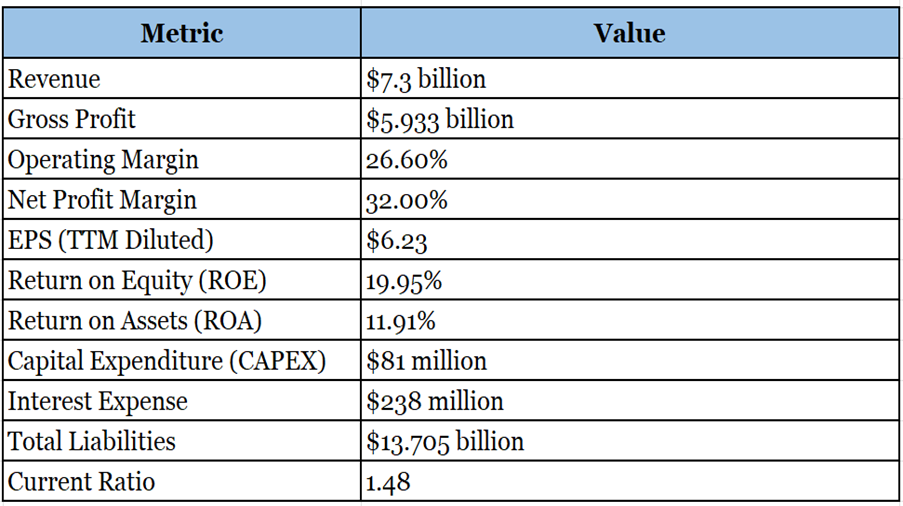

Financial Overview

- Revenue: $7.3 billion

- Net Income: $2.338 billion

- Operating Income: $1.942 billion

- Total Assets: $33.234 billion

- Total Debt: – $6.744 billion

- P/E Ratio (Current): 9.24

Key Financials

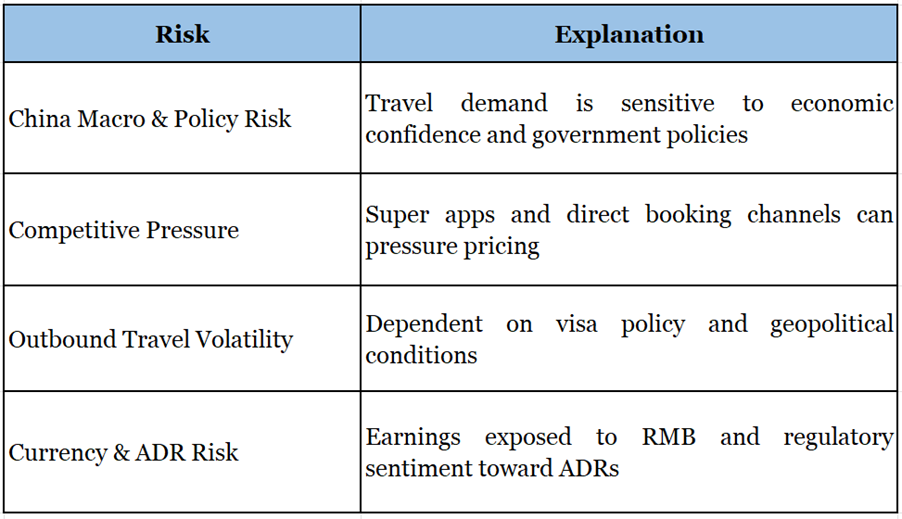

Risks

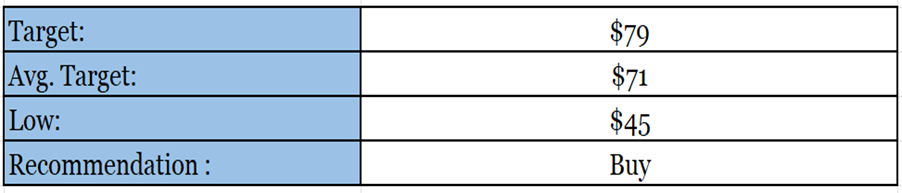

Target

Right now, the company is trading at US $57.50, with a 1-year projected target of around US $79 and a low estimation of US $45; the average price target will be US $71. The recommended buying range will be US $54 – $57.50.

MarketFacts gives a “Buy” rating on the stock at the closing price of US $57.50 as of February 10th, 2026.

Disclaimer:

The information provided in this document and the resources available for download are intended for informational purposes only and should not be interpreted as financial advice. While the content is based on thorough research and is accurate to the best of our knowledge, it is not a substitute for professional financial guidance. We strongly recommend consulting with a financial advisor to discuss your specific situation and obtain tailored advice before making any financial decisions.