Urban Outfitters, Inc.: Lifestyle Retail Platform Driven by Differentiated Brands

Company Overview

- Ticker: URBN (NASDAQ)

- Headquarters: Philadelphia, Pennsylvania, USA

- Founded: 1970

- CEO: Richard Allan Hayne

- Industry: Specialty Retail / Apparel & Lifestyle

Core Business

Urban Outfitters is a multi-brand lifestyle retailer targeting differentiated consumer segments across apparel, accessories, and home goods, with a strong omnichannel presence.

- Brand Portfolio Model: Operates distinct brands with independent design, merchandising, and customer bases, reducing reliance on any single fashion cycle.

- Direct-to-Consumer Focus: A growing share of revenue comes from e-commerce and mobile channels, improving reach and data-driven merchandising.

- Merchandising & Design Control: In-house product design allows faster trend response and higher gross margins versus wholesale-heavy peers.

- Store Network as Experience Hubs: Physical stores emphasize curated layouts and experiential retail rather than pure volume selling.

- Lifestyle Expansion: Home, wellness, and athleisure categories (especially at Anthropologie and FP Movement) diversify revenue beyond apparel.

Industry Overview

- Margin-Driven Industry: Profitability depends on refining margins (crack spreads) and regional supply-demand dynamics rather than volume growth.

- High Fixed-Cost & Operating Leverage: Capital-intensive assets create significant earnings volatility from small changes in utilization or margins.

- Supply Constraints in Developed Markets: Refinery closures, environmental regulation, and limited new capacity have structurally tightened supply.

- Cyclical Cash Flows: Periods of strong margins generate outsized free cash flow, followed by sharp downturns during margin compression.

- Long-Term Demand Uncertainty: Fuel efficiency gains and EV adoption cap long-term growth, positioning refining as a cycle-driven cash business.

Key Growth Drivers

- Anthropologie & Free People Strength: These banners consistently outperform Urban Outfitters’ core brand in margins and customer loyalty.

- FP Movement Growth: Athleisure and activewear expansion taps into a structurally growing category.

- Strong Balance Sheet: Net cash position provides flexibility during retail downturns.

- Inventory Discipline: Improved inventory management has stabilized gross margins relative to peers.

- International Expansion: Selective growth outside the U.S. offers incremental upside without heavy capital risk.

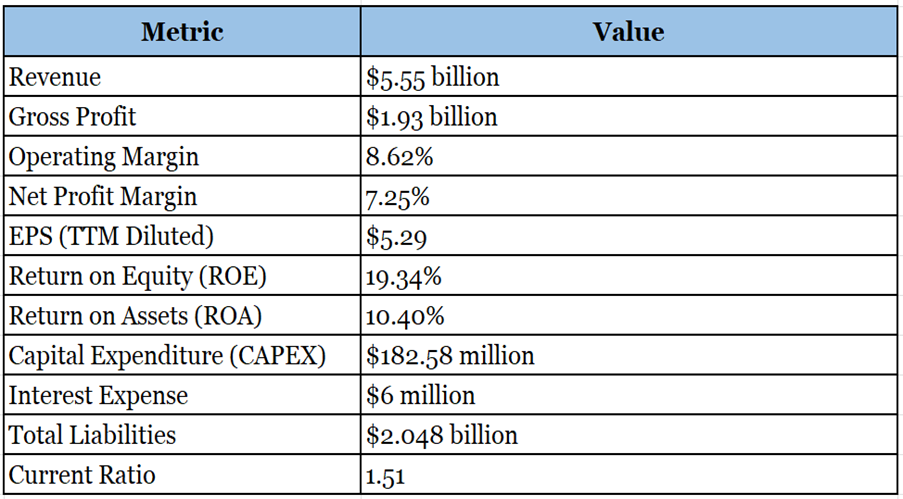

Financial Overview

- Revenue: $5.55 billion

- Net Income: $402.46 million

- Operating Income: $478.37 million

- Total Assets: $4.52 billion

- Total Debt: –

- P/E Ratio (Current): 13.72

Key Financials

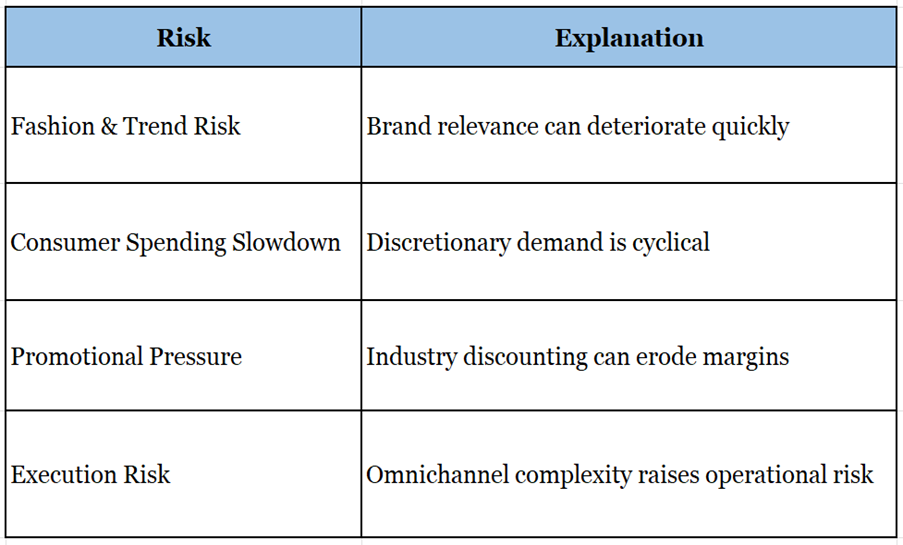

Risks

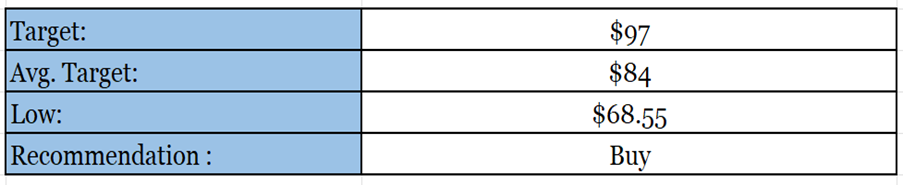

Target

Right now, the company is trading at US $73.82, with a 1-year projected target of around US $97 and a low estimation of US $68.55; the average price target will be US $84.

MarketFacts gives a “Buy” rating on the stock at the closing price of US $73.82 as of February 4th, 2026.

Disclaimer:

The information provided in this document and the resources available for download are intended for informational purposes only and should not be interpreted as financial advice. While the content is based on thorough research and is accurate to the best of our knowledge, it is not a substitute for professional financial guidance. We strongly recommend consulting with a financial advisor to discuss your specific situation and obtain tailored advice before making any financial decisions.