Stagflation Signals: Is the Global Economy Entering a More Dangerous Phase?

For much of the past year, financial markets remained focused on one dominant expectation: inflation would gradually decline, central banks would begin cutting interest rates, and global growth would stabilize. However, recent developments suggest that this outlook may be too optimistic. Rising energy prices, persistent inflationary pressures, and weakening growth indicators are reviving concerns about stagflation—a scenario markets have long feared but largely ignored.

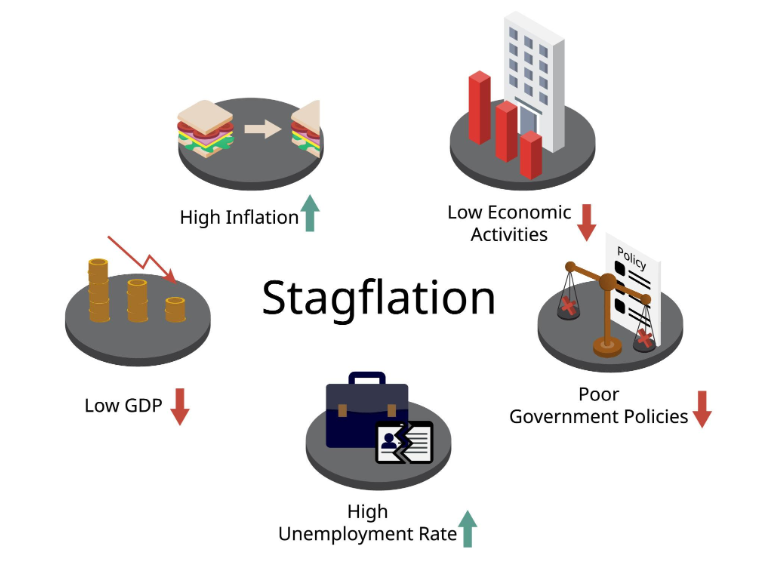

Stagflation refers to the difficult combination of slow economic growth, high inflation, and elevated unemployment or weakening labor conditions. It is considered one of the most challenging macroeconomic environments because traditional policy tools become less effective. Central banks cannot easily cut rates to support growth if inflation remains high, and tightening policy further risks pushing economies into recession.

The recent rise in oil and commodity prices has added to these concerns. Geopolitical tensions in the Middle East, supply chain disruptions, and constrained energy production have pushed energy costs higher once again. Since oil feeds directly into transportation, manufacturing, and consumer prices, higher crude prices quickly translate into broader inflation pressure across the economy.

At the same time, economic growth is beginning to show signs of fatigue. Manufacturing activity in several major economies remains weak, consumer spending is slowing under the pressure of higher borrowing costs, and business confidence is becoming more cautious. Europe faces weaker industrial demand, while China’s uneven recovery continues to weigh on global trade and commodity demand expectations.

This combination creates a dangerous policy dilemma for central banks. If inflation remains sticky because of energy prices and wage pressures, policymakers may be forced to keep interest rates elevated for longer than markets expect. However, maintaining tight monetary policy while growth slows increases the probability of a deeper economic slowdown.

Bond markets are already reflecting this tension. Rising yields suggest investors are pricing in delayed rate cuts and higher long-term inflation risks. Equity markets, however, continue to show relative resilience, creating a disconnect between financial optimism and macroeconomic caution. This divergence raises questions about whether markets are underestimating the risk of a more difficult economic phase ahead.

The comparison to the 1970s is often raised whenever stagflation fears return, though today’s environment is structurally different. Modern economies are less energy-intensive, central banks are more credible, and supply chains are more diversified. However, the core risk remains the same: when inflation and weak growth arrive together, policy flexibility becomes extremely limited.

Investors should also recognize that stagflation does not always begin with a market crash. It often develops gradually through margin pressure, weaker earnings growth, higher bond yields, and persistent volatility. Defensive sectors may outperform, while growth-sensitive and highly leveraged areas face greater pressure from tighter financial conditions.

The key issue is not whether full-scale stagflation has already arrived, but whether the early warning signs are becoming too strong to ignore. Inflation is proving more stubborn than expected, energy markets remain unstable, and global growth momentum is clearly slowing. These are not isolated events—they are interconnected signals.

The global economy may not be entering a crisis, but it is entering a more complex and potentially more dangerous phase. For investors, policymakers, and businesses, the focus should shift from hoping for a smooth soft landing to preparing for a prolonged period of uncertainty where inflation and slow growth may coexist for longer than expected.